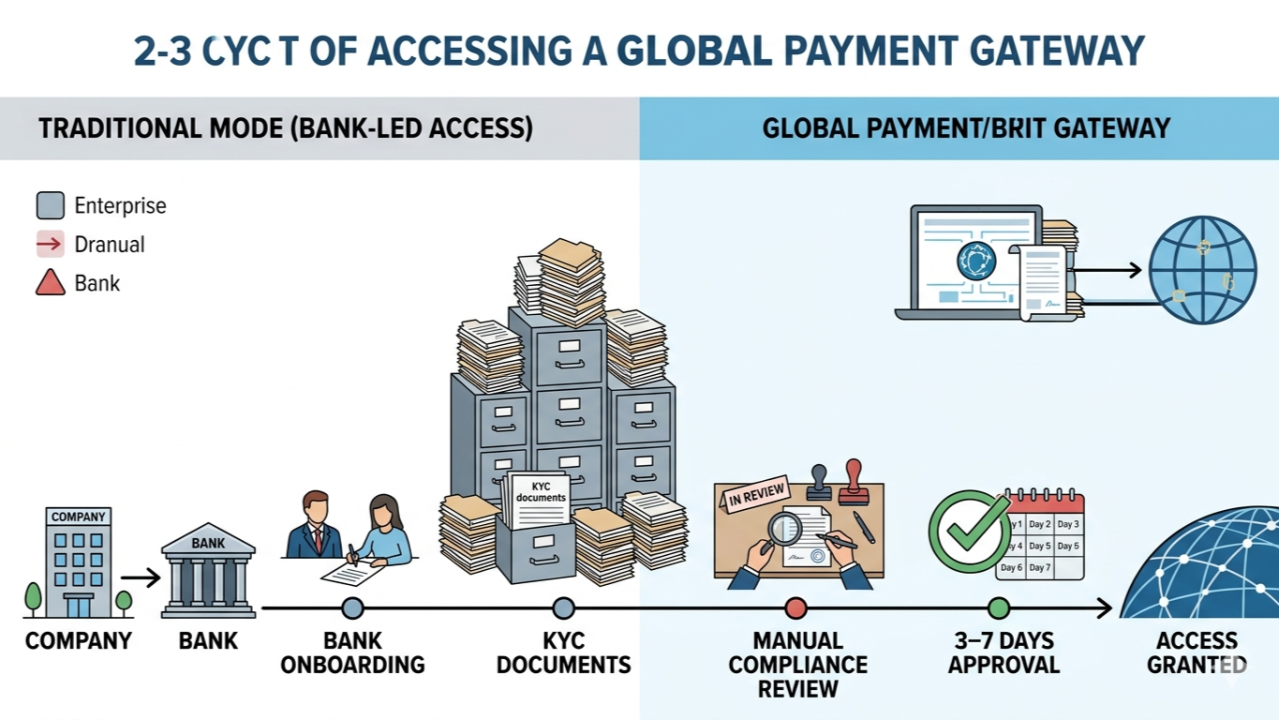

Cross-border payments have a trust problem. Every transaction crossing a border triggers identity verification, sanctions screening, and compliance checks — a process that often takes 2-5 business days and costs financial institutions billions annually. Decentralized Identity (DID) is changing this equation by replacing manual, repetitive identity checks with cryptographic, reusable verifiable credentials that work across jurisdictions.

With regulatory frameworks like eIDAS 2.0 and FATF guidance now formally recognizing DID, the technology is moving from proof-of-concept to production infrastructure. This guide explains what DID is, how it works in cross-border payment systems, and why payment providers — including Wondergate — are embedding DID into their compliance and settlement infrastructure in 2026.

What Is Decentralized Identity (DID) and How Does It Work in Payments?

Decentralized Identity (DID), defined by the World Wide Web Consortium (W3C), allows individuals and institutions to present verifiable credentials — proof of identity, business registration, regulatory compliance — without relying on a centralized identity authority. Instead of a bank in Singapore calling a bank in Germany to verify a corporate customer, both parties rely on cryptographically signed credentials stored on a decentralized ledger.

With the release of DID v1.1 and Verifiable Credentials (VC) 2.0, the W3C established a global interoperability baseline specifically designed for financial services adoption. Three core components make this possible:

- Decentralized Identifiers (DIDs): Globally unique, persistent identifiers not tied to any central registry — controlled entirely by the identity owner.

- Verifiable Credentials (VCs): Tamper-proof digital attestations (e.g., "this entity passed KYC") signed by trusted issuers and verifiable by anyone.

- Zero-Knowledge Proofs (ZKPs): Cryptographic methods that enable selective disclosure — proving you are over 18 without revealing your birth date, or proving KYC clearance without exposing your full identity documents.

| Factor | Traditional KYC | DID-Based Identity Verification |

|---|---|---|

| Verification Speed | 2-5 business days | Minutes |

| Re-verification Per Market | Required for each jurisdiction | Single credential, multi-jurisdiction |

| Compliance Cost | High (manual, repetitive) | 45% lower |

| Data Privacy | Full identity documents shared | Selective disclosure via ZKP |

| Fraud Prevention | Reactive, document-based | Cryptographic, 57% fewer incidents |

| Market Entry Barrier | High (per-jurisdiction compliance) | 60%+ reduction |

How Does DID Reduce KYC Time and Compliance Costs in Cross-Border Payments?

The traditional KYC process for cross-border payments is remarkably inefficient: the same corporate entity must undergo separate KYC procedures for every payment corridor, every correspondent bank, and every jurisdiction — even though the underlying identity information does not change. DID eliminates this redundancy.

More than 30 major banks have now integrated DID standards into their cross-border payment infrastructure upgrades. The results are significant:

- KYC cycles dropped from 2-5 business days to minutes

- Repetitive jurisdictional checks eliminated — one DID credential works across all corridors where the issuer is trusted

- Overall compliance costs reduced by 45%

- Compliance reporting efficiency improved by 70%

- Fraud incidents decreased by 57% through cryptographic verification replacing document-based checks

For payment providers, this is not just a compliance win — it is a competitive advantage. Faster onboarding means faster time-to-revenue for merchants, and lower compliance costs improve unit economics at scale.

What Regulatory Frameworks Are Recognizing DID for Cross-Border Payments?

For DID to work in regulated financial services, it needs legal recognition — and 2025-2026 has delivered exactly that through two landmark frameworks:

eIDAS 2.0 and the EU Digital Identity Wallet: The European Union's revised electronic identification framework now legally recognizes DID-verifiable credentials across all 27 member states. The EU Digital Identity Wallet — rolling out through 2026 — enables citizens and businesses to store and present DID-based credentials for financial services, including cross-border payment verification. Critically, non-EU providers can now access the EU market through a single trusted identity layer, removing the need for per-country compliance registrations.

FATF Travel Rule Guidance: The Financial Action Task Force (FATF) now explicitly recognizes DID as compliant with Travel Rule requirements for cross-border transactions. This means DIDs can satisfy the originator and beneficiary information requirements that apply to cross-border wire transfers — a crucial step for mainstream adoption in correspondent banking.

These regulatory developments are part of a broader structural shift in global payment infrastructure. For context, see our analysis: Global Payments System Shift: Regulation, AI & CBDCs.

How Is DID Replacing Correspondent Bank Trust With Cryptographic Verification?

Correspondent banking has always been built on bilateral trust relationships — Bank A trusts Bank B because they have a long-standing relationship, contractual agreements, and mutual regulatory compliance. This model works but it is slow, expensive, and excludes institutions without established correspondent networks.

DID replaces this relationship-based model with cryptographic trust:

- Instead of a 6-month correspondent banking onboarding process, an DID credential can be verified in seconds

- Payment networks across Africa and ASEAN are using DID for cross-jurisdiction identity mutual recognition

- Market entry barriers for payment providers entering new corridors have dropped by over 60%

This is particularly impactful in emerging markets, where correspondent banking relationships are thinnest. DID provides a cryptographic shortcut — enabling smaller financial institutions and payment providers to participate in cross-border payment networks without the traditional multi-year relationship-building timeline.

Why Are Payment Providers Becoming Identity-Compliance Platforms?

The DID financial services market reached $1.52 billion in 2025, with over 60% of adoption driven by cross-border payments. This growth signals a fundamental shift in what payment providers are becoming: not just transaction channels, but identity-compliance platforms.

62% of leading payment providers are now embedding DID into their settlement infrastructure. The logic is straightforward: if a payment provider already handles KYC for transaction compliance, extending that capability into a reusable, portable identity credential creates network effects. Each DID-verified merchant or institution becomes easier to onboard across new corridors, new currencies, and new regulatory regimes.

For businesses that process cross-border payments, this trend means selecting a payment provider is increasingly a decision about identity infrastructure — not just transaction processing. A provider with embedded DID capability shortens your time-to-market in new jurisdictions by eliminating redundant compliance onboarding. For a practical introduction to how payment infrastructure works end-to-end, see: What is a Payment Gateway? A Complete Guide.

What Are the Most Common Misconceptions About DID in Financial Services?

Misconception 1: "DID is the same as blockchain-based identity." While DIDs are often stored on decentralized ledgers, the DID standard (W3C) is ledger-agnostic. It can work with blockchains, traditional databases, or hybrid architectures. The key innovation is the verifiable credential model, not the storage technology.

Misconception 2: "DID means full transparency — everyone can see identity data." Zero-knowledge proofs enable selective disclosure. A payment provider can verify that a merchant passed KYC without ever seeing the underlying identity documents. This is a privacy-preserving model, not a transparency model.

Misconception 3: "Regulators will not accept DID because it is too new." eIDAS 2.0 and FATF guidance already provide legal recognition. The regulatory framework is ahead of many financial institutions' implementation timelines — the bottleneck is adoption, not regulation.

Misconception 4: "DID only matters for KYC — it does not affect payment processing." Identity is the gateway to payment processing. Faster identity verification means faster merchant onboarding, faster settlement, and fewer false-positive compliance flags that block legitimate transactions. DID's impact on payment processing is indirect but material — especially for businesses entering new markets.

Frequently Asked Questions

Q: What is the difference between DID and traditional digital identity?

A: Traditional digital identity relies on a central authority (e.g., a government or bank) to issue and verify credentials. DID uses decentralized identifiers and verifiable credentials that can be verified cryptographically without querying a central database. This means credentials work across borders and institutions without depending on bilateral trust relationships.

Q: Is DID legally recognized for cross-border payment compliance?

A: Yes. The EU's eIDAS 2.0 framework legally recognizes DID-verifiable credentials across all 27 member states. FATF guidance explicitly recognizes DID as compliant with Travel Rule requirements for cross-border transactions. These frameworks provide the legal foundation for financial services adoption.

Q: How much can DID reduce KYC costs?

A: Financial institutions implementing DID report a 45% reduction in overall compliance costs, a 70% improvement in reporting efficiency, and KYC cycle compression from 2-5 business days to minutes. These savings come from eliminating repetitive jurisdictional checks and enabling a single credential to satisfy compliance across multiple payment corridors.

Q: Does DID compromise data privacy?

A: No — DID with zero-knowledge proofs enhances privacy by enabling selective disclosure. A verifier can confirm that a credential is valid (e.g., "KYC passed") without accessing the underlying identity data. This contrasts with traditional KYC where full identity documents must be shared with every new institution.

Q: Which regions are adopting DID fastest for cross-border payments?

A: The EU leads through eIDAS 2.0 and the Digital Identity Wallet rollout. Africa and ASEAN are also strong adopters, using DID for cross-jurisdiction identity mutual recognition — particularly valuable in regions with limited correspondent banking networks. Over 30 major banks globally have integrated DID into their cross-border payment infrastructure.

Q: How does DID relate to the broader evolution of payment infrastructure?

A: DID is part of a larger structural shift in global payments — alongside RTGS adoption, ISO 20022 messaging, AI-driven compliance, and CBDC experimentation. These technologies are collectively replacing the legacy correspondent banking model with real-time, cryptographic, and programmable infrastructure. See our analysis of this broader transition: Global Payments System Shift: Regulation, AI & CBDCs.

Decentralized Identity is redefining how trust, compliance, and market access operate in global cross-border payment systems. As regulatory frameworks solidify and implementation accelerates — from 30+ banks today to an expected 100+ by 2027 — DID will move from a competitive differentiator to a baseline requirement. Payment providers that embed DID into their infrastructure today are building the compliance layer that will define market access for the next decade.

To learn how Wondergate integrates identity, compliance, and settlement into a unified cross-border payment infrastructure, explore our global payment solutions.